Hospital Plan Guide: What to Look For (and How the Schemes Rate)

What a hospital plan covers, how it differs from full medical aid, what to look for, and how South Africa's major schemes rate on customer experience.

Hospital Plan Guide: What to Look For (and How the Schemes Rate)

A hospital plan is the most affordable way to protect yourself against the big, expensive medical events, a hospital admission, surgery, or a serious diagnosis. It is also one of the most misunderstood products in South Africa, because "hospital plan", "medical aid" and "hospital cash plan" get used as if they mean the same thing. They do not.

This guide explains what a hospital plan actually covers, how it differs from full medical aid, what to look for before you commit, and how the major schemes rate on customer experience based on Hellopeter's analysis of real member reviews. One thing up front: a low experience score is not the same as bad cover. It tells you how a scheme treats members on claims, communication and admin, which is exactly where most of the frustration sits.

What a hospital plan actually covers

A hospital plan covers your in-hospital costs: the ward, theatre, the surgeon and anaesthetist, and related in-hospital treatment. By law, every registered scheme option must also cover the Prescribed Minimum Benefits (PMBs), a regulated list of around 270 conditions plus a set of chronic conditions and emergencies that all schemes have to fund regardless of the plan you choose.

What a hospital plan generally does not cover is day-to-day care: GP visits, dentistry, optometry, and over-the-counter or non-PMB chronic medication. Those come out of your own pocket unless you add a savings or day-to-day benefit, which moves you toward a fuller (and pricier) medical aid plan.

Hospital plan vs full medical aid vs hospital cash plan

These three are easy to confuse, and the difference matters:

- A hospital plan is a medical scheme option that covers in-hospital costs and PMBs. It is regulated medical aid, just a more affordable tier.

- A full (comprehensive) medical aid adds day-to-day cover, savings, and broader benefits. It costs significantly more.

- A hospital cash plan is not medical aid at all. It is an insurance product that pays you a fixed cash amount per day in hospital. It will not cover a large hospital bill, so it is a top-up, never a replacement for a hospital plan.

If your goal is to be protected against a major medical event without paying for full cover, a hospital plan is usually the product you are looking for, not a cash plan.

Why you probably also need gap cover

This is the part most people only discover when the bill arrives. A hospital plan pays your in-hospital costs at the medical scheme rate. But private specialists, surgeons and anaesthetists often charge several times that rate. Your scheme pays its portion, and you are left with the shortfall, which on a major procedure or a hospital birth can run to thousands or even tens of thousands of rands.

Gap cover is a separate, relatively affordable insurance product that bridges exactly this gap. It pays the difference between what a specialist charges for in-hospital treatment and what your scheme covers, and many plans also help with co-payments and certain sub-limits. It is not medical aid and cannot replace your hospital plan, you need a scheme to have gap cover, but for anyone using private hospitals it is often the difference between a covered procedure and a frightening bill. There is an annual limit on what gap cover pays, set by regulation and adjusted each year, and waiting periods can apply, so read the terms before you need to claim.

The simplest way to think about it: a hospital plan protects you against the hospital's bill, and gap cover protects you against the specialists' shortfall. Most people who use private healthcare want both.

What to look for before you commit

Once you know you want a hospital plan, compare options on these points rather than on the brand name:

- The hospital network. Some plans cover any private hospital; cheaper options restrict you to a network, and going outside it can mean large co-payments. Check which hospitals near you are covered.

- Co-payments. Many plans have co-payments on specific procedures (scopes, scans, certain surgeries). Ask for the co-payment list before you join.

- Waiting periods and late-joiner penalties. A new member can face a three-month general waiting period, a twelve-month wait on pre-existing conditions, and, if you join a scheme later in life, a permanent late-joiner penalty. These are normal and regulated, but you need to know them upfront.

- Chronic and PMB cover. Confirm how the plan handles chronic medication for PMB conditions, and whether it pushes you to a specific pharmacy or generic.

- Whether you also need gap cover. Because a hospital plan only pays at scheme rates, factor gap cover into your budget to bridge specialist shortfalls (see above), especially if you use private hospitals.

- How claims and authorisation work. This is the one most people skip, and the data below shows it is exactly where schemes fail.

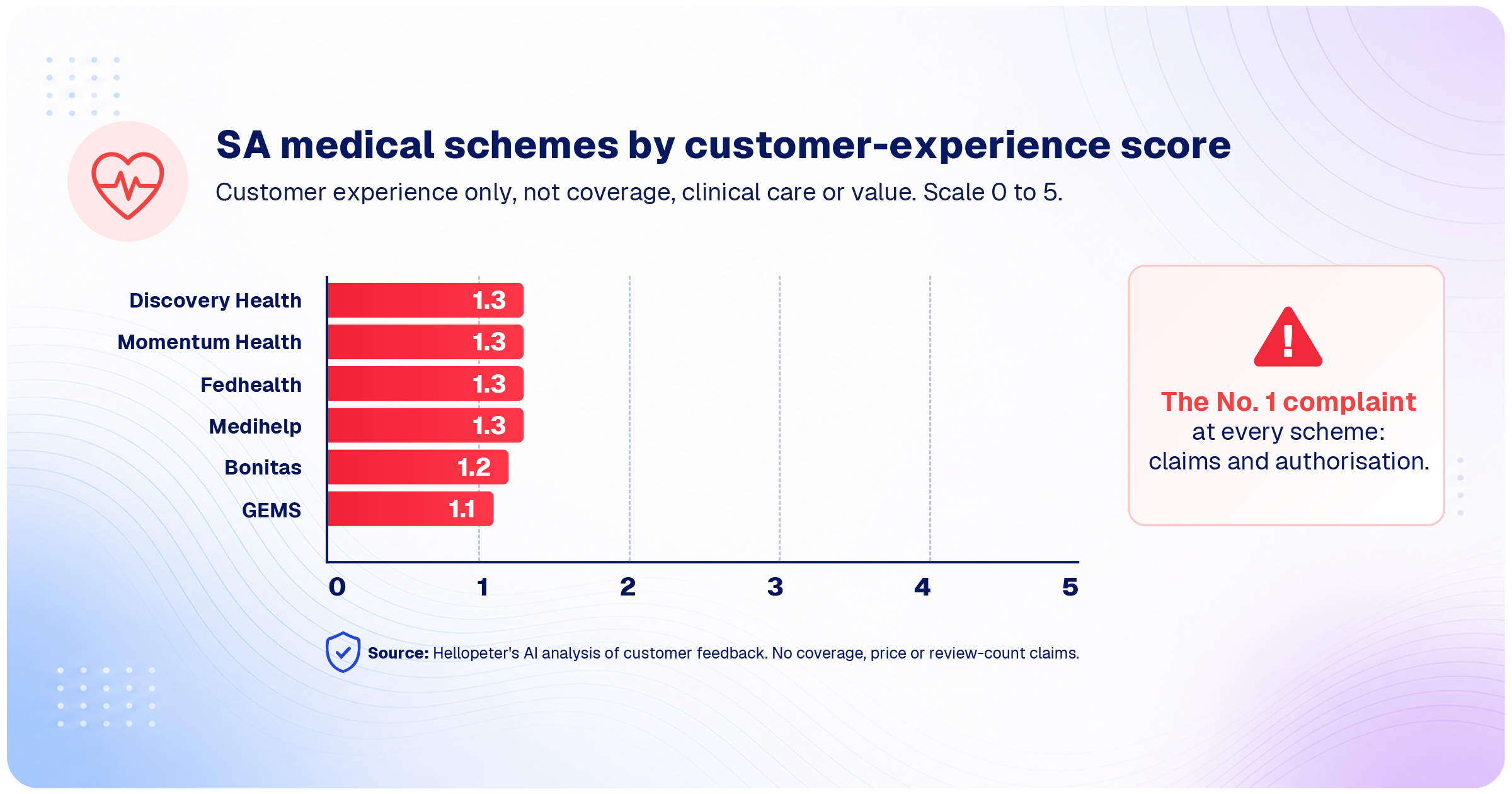

How the major schemes rate on customer experience

The table below is based on Hellopeter's AI analysis of member reviews. It measures customer experience only, how the scheme handles claims, communication and admin, not the quality of clinical care, the cover itself, or value for money. The striking thing is how little separates them: experience scores are low across the board, and the same issue, claims and authorisation, drives the complaints almost everywhere.

| Scheme | HP experience score | Most-flagged issue |

|---|---|---|

| Discovery Health | 1.3/ 5 (Terrible) | Service and rejected claims |

| Momentum Health | 1.3/ 5 (Terrible) | Claims and authorisation |

| Fedhealth | 1.3/ 5 (Terrible) | Claims and authorisation |

| Medihelp | 1.3/ 5 (Terrible) | Rejected claims and co-payments |

| Bonitas | 1.2/ 5 (Terrible) | Claims and authorisation |

| GEMS | 1.1/ 5 (Terrible) | Claims and authorisation delays |

Source: Hellopeter's AI analysis of customer feedback (experience only, not coverage or value) — June 2026

Because the scores are so close, the brand is not the deciding factor. The deciding factor is fit (does the plan cover the hospitals and conditions you need) and how the scheme handles a claim when it counts. That is what to test.

The one thing to pressure-test: claims and authorisation

Since claims and authorisation is where every major scheme draws the most complaints, make it your interview question before you sign. Ask: how do I get pre-authorisation for a planned procedure, and how long does it take? What are the most common reasons claims get rejected? How are co-payments communicated before treatment, not after? How is chronic medication for a PMB condition approved? A scheme that answers these clearly and in writing is telling you something useful. One that cannot is showing you the problem before you have paid a cent.

What to do if a claim is wrongly rejected

If a claim or authorisation is unfairly declined, you have rights. Put your dispute to the scheme in writing and ask for the specific clause they are relying on. If they will not resolve it, you can escalate to the Council for Medical Schemes (CMS), the industry regulator, which handles member complaints against schemes. Putting your experience on the public record on Hellopeter also helps, both to move your own case and to inform the next person. For the full step-by-step approach, see our guide on how to complain effectively.

A Note on This Article

Hellopeter is independent and impartial. We are not affiliated with the schemes mentioned, and nothing here is sponsored. Everything below is based on public, verified customer reviews on Hellopeter, which change as new reviews come in, so the figures reflect the picture at the time of publication. This is general information to help you compare, not financial advice, so do your own research before you decide.

Frequently asked questions

- Is a Hospital Plan Worth It?

- For most people who want protection against a major medical event without paying for full cover, yes. It covers the costs that would otherwise be financially devastating, a hospital admission or surgery, plus the regulated PMBs. It will not cover everyday GP or dental visits.

- Do I Need Gap Cover as Well as a Hospital Plan?

- If you use private hospitals and specialists, almost certainly. A hospital plan pays at scheme rates, but specialists often charge several times more, and gap cover bridges that shortfall, the same shortfall that catches many people out after a procedure or a hospital birth. It is a separate, affordable product, not a replacement for your plan, so budget for both.

- What Is a PMB?

- Prescribed Minimum Benefits are a regulated set of conditions, including emergencies and a list of chronic conditions, that every medical scheme option must cover by law, no matter how basic the plan. If a scheme refuses to fund a PMB, that is grounds to escalate.

- Does a Hospital Plan Cover Chronic Medication?

- It covers chronic medication for PMB-listed conditions. Medication for non-PMB conditions is usually not covered on a hospital plan, so check the chronic list against your own needs.

- What Is the Difference Between a Hospital Plan and a Hospital Cash Plan?

- A hospital plan is medical aid that pays your in-hospital bill. A hospital cash plan is insurance that pays a small fixed amount per day in hospital. A cash plan will not cover a big hospital bill, so it is a top-up, not a substitute.